Outlook 2022: Have Valuations Peaked?

![]()

While U.S. M&A activity in the first quarter of 2022 declined from near-record levels of a year ago, ongoing near-term interest in acquisitions could well be sufficient to muscle aside concerns over inflation, ongoing labor and supply chain issues, and the prospect of higher interest rates. However, the confluence of a number of these factors could lead to a pullback in valuations – which may in turn result in some potential sellers either remaining on the sidelines or failing to transact due to inflated value expectations.

A Historical Perspective

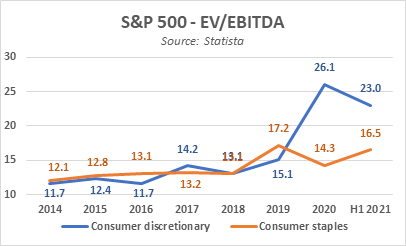

In the equity markets, a recent study by Bain & Co. concluded that multiples expansion was the primary driver of increased public company valuations, over margin expansion and sales growth, by a considerable margin. Enterprise values in the Consumer Discretionary sector illustrate the degree to which multiples have grown in the presence of low rates, and their vulnerability in the face of headwinds from the Fed. Acquisition multiples have exhibited similar trends, particularly for growth assets.

Current Environment Relevant to Pricing Deals

Those most optimistic on the outlook for M&A multiples will cite the near-record levels of cash available for acquisitions, among both private equity and corporate purchasers, which should help sustain competition, especially for high-quality targets. However, deal pricing is likely to be affected by a variety of financial, geopolitical and operational factors, including the following.

Financing Costs

Despite the relative strength of investor balance sheets, most deals are funded with a debt component, rendering the impact of rates on an M&A transaction particularly meaningful. In today’s environment, a 100-basis point increase in the cost of capital for acquisitions (as measured by long-term treasuries as well as corporate borrowing costs) may have a 200-basis point reduction in the value of a target’s cash flows (as a multiple of EBITDA), absent any other forecast adjustments. Intangible factors can also come into play, particularly among business owners already financing surplus working capital to ensure supply, who may become more cautious in their views on valuation and whether to burden the operation with added leverage.

Forecasting in the Face of Ongoing Supply Chain Challenges

Lost business from supply disruptions historically could be rationalized as temporary “hiccups” in execution. A business being sold might reflect adjustments for lost revenue or added costs on the notion the disruption was a nonrecurring event. Earlier this month, however, the U.S. Census Bureau reported that February unfilled orders for manufactured durable goods increased for the thirteenth consecutive month, while the near-term outlook is at a heightened risk from recent COVID-related lockdowns in China – both of which highlight the importance of supply chain diligence in developing an acquisition forecast.

Forecasting in the Face of Volatility in Demand

In addition to supply-side challenges, we remain in an environment where demand volatility has been historically high, rendering it difficult to forecast one’s own business, let alone that of a potential target. In many consumer sectors we are seeing the anniversary of a two-year COVID cycle, whereby an extraordinary impact on demand (positive or negative) has been followed by a significant correction. In hand hygiene, for example, demand more than doubled prior to the rollout of vaccines, while usage of various personal care categories declined significantly during periods of isolation, in both cases only to revert to historical norms.

Implications

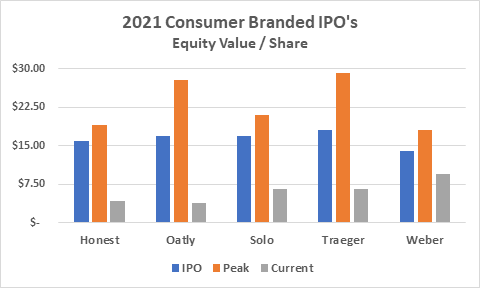

Turning again to the public markets, we can illustrate the magnitude of valuation resets in five growth-oriented consumer branded companies which completed Initial Public Offerings in the past twelve months and who have been affected by supply chain issues or a rebasing of expectations following COVID-induced category (or channel) demand surges. On average, the firms have lost in excess of 60% of their IPO value (and nearly 75% from their peaks), in some cases despite still favorable long-term outlooks.

Inexpensive capital may permit chasing growth with aggressive valuations – but the outcomes below also highlight the risks from any resetting of forecast expectations. And while an investor in a broad equity portfolio may be able to absorb an occasional miss, excess exuberance of this magnitude isn’t something a privately-held cash buyer of a going concern can easily afford to make.

In an environment where business projection risks remain high and capital costs are increasing, the need for a thorough diligence process and a thoughtful business plan is particularly acute. Potential purchasers will need to assess the degree to which growth may or may not be sustainable from behavior changes, favorable demographic factors, or from share gains. They may also need to ask whether growth should inherently be considered episodic (for example, in categories driven by climate change events or, in the case of hand sanitization, viral outbreaks) as well as the degree to which growth or margins may be suppressed by supply chain factors. And, in the presence of declining M&A multiples it is important to keep in mind that the ability to reach a completed transaction may be temporarily affected by resistant seller value expectations. A successful outcome may require supplementing your team’s capabilities with trusted professionals wherever a potential transaction is material, or of critical importance, to the firm.